Landlords against startups & the birth of VC

Startup Culture: Analysis, history & field notes from Silicon Valley.

Entrepreneurs versus Rentiers

Two of the most interesting Twitter conversations (and by far the best op-ed column) to come out of Silicon Valley last week had a common theme: startup founders struggling in the Bay Area housing market.

From Paul Graham, a reminder that Airbnb “happened because its founders literally could not pay their rent:”

And from Austen Allred of Lambda School, a hustle-inspiring tale of, well, homelessness:

You can read the whole thread to see how this turned out. What’s more important is how these conversations fit into the much wider question of housing in San Francisco and Silicon Valley. Most of the replies to Paul’s tweet focussed on the question of whether you need to be rich to start a startup—when really, we should be asking what founders need all that money for.

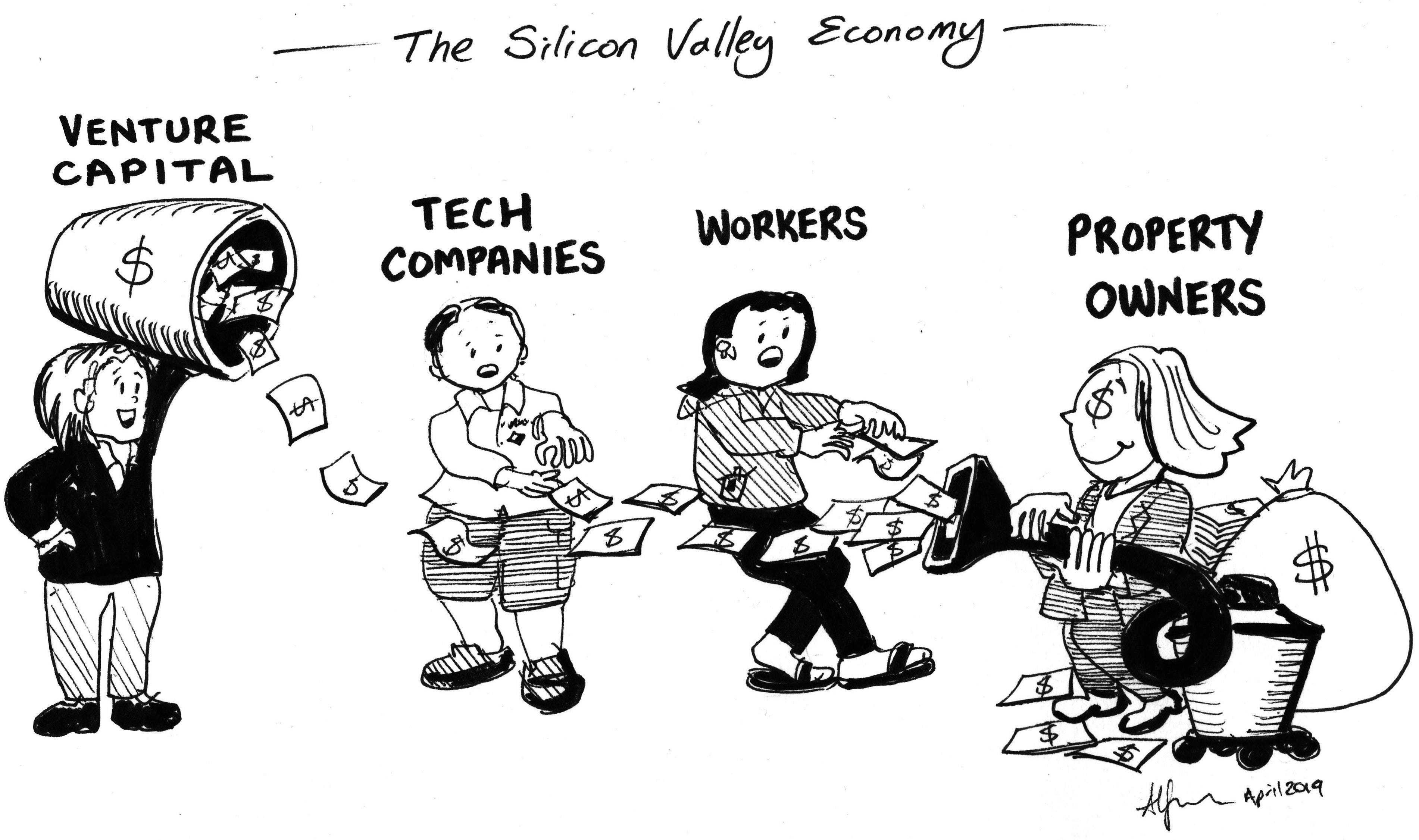

Not surprisingly, it’s rent. A cartoon by Alfred Twu in the Bay City Beacon summed up the problem beautifully:

Unless, like Austen, you live in your car (which more and more cities are making illegal), there’s a good chance most of your money will be going straight to a landlord in the early months (if not years) of your startup.

It’s ironic that the world’s greatest entrepreneurial economy is based in what Joseph Schumpeter would have seen as a “rentier city.” Schumpeter, whose ideas of creative destruction and entrepreneurial spirit shaped the first venture capitalists’ thinking, characterized the rentier state as one based on old money, static routines and the stagnation of development. Throughout the history of innovation, economists have emphasized that rentier capitalism is directly opposed to entrepreneurship, but I don’t know of any historical parallels to what’s happening in San Francisco right now: the capture of a huge share of new, technology-generated wealth by residential real estate owners.

It was interesting to see how many VCs wanted to boost the idea that property owners are the biggest barrier to innovation today. While some asked what the difference was between speculating on real estate and founding a startup, it seems pretty clear to others: property owners aren’t doing anything new, so they aren’t entrepreneurs.

Looking more closely at this situation through the lens of his model of economic development, it’s clear Schumpeter would agree:

there are three ways in which the transition from… a given state of the economy to another state takes place, in which the “data of the equilibrium state” change, and in which “economic development” takes place: first, through continuous growth, in particular of the population and...means of production. Second, through extra-economic events that permeate the economy... Third, because some individuals recognise and carry out new possibilities within the given circumstances of economic life, possibilities that extend beyond economic experience and tried and familiar routine.

In case you were wondering, breaking records for the cost of an apartment doesn’t count as extending economic experience. In these terms, property owners are profiting from the growth in (local) population driven by new tech jobs, and political “events” like the rejection of pro-housing policies, but the source of this wealth is really the work of a different class: the innovator and entrepreneur.

There’s a big difference between San Francisco and Silicon Valley cities and Schumpeter’s classic “rentier state,” however. Instead of the state extracting tax revenue from the productive segments of the economy (and keeping the populace more-or-less happy by redistributing the proceeds in one way or another), thanks to decades of legislation and policymaking that have served property owners’ interests at the cost of education, social services and infrastructure, and choked off California’s supply of new housing, the rentier cities of the Bay Area funnel money directly to landlords and homeowners.

Instead of paying taxes on their profits, entrepreneurs pay rent (in both the everyday and economic senses) to Bay Area property owners just for the chance to start a startup where it’s most likely to be successful.

Entrepreneurs are all too often seen as the source of the Bay Area’s housing crisis. The numbers don’t add up, though: according to CBInsights, just 677 seed or angel stage companies were funded in San Francisco in 2018. Even assuming not every deal is recorded there, over the same time, the city added another 25,000 tech jobs in established companies—most of them probably a good deal better paid than founders’ salaries.

There simply aren’t enough people working on early-stage startups to move the needle. But they still pay the price of living in a region where the productive part of the economy is held hostage by unproductive real estate capital. What Bay Area landlords and homeowners are really making money from is renting access to the “regional advantage” of the real-world social network of Silicon Valley and the SF tech industry. While venture capital and hiring practices might adapt to survive this constant drain, in the long term, the quality of this network—and the ventures it spawns and supports—will inevitably decline.

Against this backdrop, Farhad Manjoo’s excellent column comparing Trump’s border wall and the “wealthy liberal elites” of San Francisco and other cities’ exclusionary, anti-housing policies couldn’t have been better timed.

What Republicans want to do with I.C.E. and border walls, wealthy progressive Democrats are doing with zoning and Nimbyism. Preserving “local character,” maintaining “local control,” keeping housing scarce and inaccessible — the goals of both sides are really the same: to keep people out.

If there’s one thing he misses, though, it’s the huge profits that Bay Area property owners make from housing being so scarce and inaccessible. In a way that just isn’t true of immigration policy, keeping housing unaffordable puts real money in the pockets of wealthy “progressives” (and the decidedly less progressive population of landlords!).

It’s going to be interesting to see if the opposition between the two kinds of capital which have reaped the rewards of Silicon Valley’s success—one productive, one parasitic—will lead to real change in housing policy. On one hand, the tech industry (and especially venture capital) could take a more active role in lobbying for progress at a local level: from individual fund returns to national competitiveness, there’s almost as strong a case for making rent affordable for entrepreneurs (and everyone else!) as there is for rational (and humane) immigration policies.

I’m not optimistic for this outcome yet. The incentives for entrenched (property-owning) interests to maintain the status quo are probably just to high for even the best-funded campaign to overcome.

It looks more likely that the combination of remote/distributed teams, combined with the increasing difficulty of recruiting in the Bay Area, will push many entrepreneurs out of the region (or stop them moving there in the first place). While that may be good for the startup ecosystem in many ways, particularly if it helps burst the bubble of entrepreneurs solving a narrow range of “first world problems,” there is, I think, reason to be concerned that the disruption and degradation of Silicon Valley’s face-to-face social networks may have serious negative effects on the development of new ventures—particularly in technology-intensive fields like AI and biotechnology.

SV History: The Invention of Venture Capital

The Oxford English Dictionary tells us that venture capital is the same thing as risk capital, and that the term was first used in 1943. I’m sure most readers will take issue with the first part. I found that the term has a much longer, and quite surprising history.

Given the distance, literal and otherwise, between Wall Street and Sand Hill Road, it’s pretty ironic that the earliest record of the use of the term venture capital is in a report presented by Harold Stanley, then Vice President for bonds at the Guaranty Trust Company of New York (and later co-founder of Morgan Stanley!), to the 1920 meeting of the Investment Bankers’ Association:

...the placing of speculative securities is a most important element of corporate financing. The enlistment of venture capital is necessary for the development and growth of the country, as well as for the safety of all investment securities.

For the next eighteen years, the term seems to be scarcely used (and then largely in accounting texts) until it is taken up by Lamott du Pont II, then-President of the E.I du Pont de Nemours chemical company. He brought up venture capital in response to a question posed by Sen. James F. Byrnes, the Chairman of the Senate Special Committee to Investigate Unemployment and Relief (and an enthusiastic New Deal proponent) about the supply of capital for new industrial ventures.

du Pont made his point at a meeting of the Senate committee held on 10th January, 1938:

“You get the difference between venture capital and borrowed money? You may be able to create credit, which is borrowed, but that is not venture capital.”

Byrnes asked him to clarify what he meant by this term, and the definition Stanley gives is one which is easily recognizable even today:

MR. DU PONT: By “venture capital” I mean that capital which will go into an enterprise and not expect an immediate return, but will take its chances on getting an ultimate return.

SENATOR MURRAY: From where does that kind of capital come?

MR. DU PONT: It will come, originally, from savings, but my judgment is that venture capital must be supplied, either by aggregations of wealth, or wealthy persons, because it is only the persons of reasonable wealth who can justify taking the risk of the venture.

The editors of the Wall Street Journal marked the occasion of his comments with a short, typically anonymous column entitled Two Kinds of Capital: they found it a “peculiarly happy phrase to describe the type of capital investment which has been lacking for several years,” namely “investment without definite assurance that the funds will produce, at the outset, income commensurate with the commitment.”

So then, the term venture capital has a history which reaches back almost a century, and from its early days, we can already recognize its distinctive qualities (like the insistence that only the wealthy can supply it, later codified in the SEC’s “accredited investor” status).

Links

Why Hasn’t an Occupy White House Emerged?

An interesting question from superstar investor Hunter Walk: “what type of outrage or frustration could catalyze an ongoing Occupy community, one that might even be 10x larger or more durable?”

San Francisco boasts world's highest salaries amid rising homelessness

A story which got surprisingly little attention on SV Twitter, for some reason. Good news for (some) workers. Not so good for founders. And as we’ve seen, great for property owners.

The Meaning Machine

A long read from one of the most interesting thinkers in the consciousness enhancement, AI and posthumanism space.

The things that we find to be meaningful are, in fact, miniature Experience Machines. They rely on illusion and filter the information that reaches us so that we may continue to feel that life is meaningful, or continue to search for meaning in life if it is missing. They are very useful; they help us organize our behavior, coordinate with others, and manage our emotions. In a practical sense they often make the suffering of life bearable; but, once they are recognized to be illusions, they cannot justify suffering in an abstract sense any more than pleasure can.